Editors’ note: This article is Andrew Kliman’s response to David Harvey’s recent criticisms of Marx’s theory of capitalist economic crisis. It was originally published in New Left Project; Part 1 appeared on March 10, 2015 and Part 2 appeared on March 12.

On Douglas Lain’s podcast, Zero Squared, he and Kliman discussed the article, the environment of “Marxist entertainment” in which errors such as those made by Harvey are common and flourish, and whether Marx’s crisis theory has practical political consequences. The hour-long discussion was preceded by a short clip in which Brendan Cooney talks about the Marx’s law of the tendential fall in the rate of profit, in which his crisis theory is rooted. You can listen to the podcast here.

Harvey versus Marx on Capitalism’s Crises

by Andrew Kliman

Part 1: Getting Marx Wrong

David Harvey, a well-known Marxist geographer, recently published a draft paper (Harvey 2014) that vigorously criticises Karl Marx’s ‘law of the tendential fall in the rate of profit’ (LTFRP), its place within Marx’s theory of capitalist economic crisis, and its relevance to the Great Recession and the recession’s prolonged aftermath. The law says that the rate of profit tends to fall because of labour-saving technological progress under capitalism. By lowering costs of production, technological innovations tend to keep products’ prices from rising, and this makes it difficult for companies’ profits to increase as rapidly as the amount of capital they invested to produce their products.

Whether this process was among the underlying causes of the Great Recession is a matter of great political importance. At issue is whether policies intended to make capitalism work better—replacement of neoliberalism with statist capitalism, financial regulation, reduced inequality, policies that favor production over finance, and so on—can succeed in preventing major economic crises in the future. The theory of crisis rooted in the LTFRP suggests that such policies cannot ultimately be successful, because they leave intact the drive to maximize profit and the link between technological progress and falling profitability, which are part and parcel of every form of capitalism.

Harvey’s chief complaint is that the LTFRP and the theory of crisis based on it are mono-causal: it ignores other causes of crisis as well as counteracting factors, and its current proponents typically present it in a way that ‘exclude[s] consideration of other possibilities’. I will argue that this is just a strawman.

The real issue is not that anyone has advocated a mono-causal theory, but that Harvey is campaigning for what we might call an apousa-causal theory, one in which the LTFRP plays no role at all (apousa is Greek for ‘absent’). He is the one who is trying to exclude something from consideration. In light of his emphasis on capitalism’s ‘maelstrom of conflicting forces’ and its ‘multiple contradictions and crisis tendencies’, one might expect that he would urge us to consider all potential causes of crisis, excluding nothing. However, Harvey is not merely suggesting that other potential causes of crisis be considered alongside the LTFRP. He seems determined to consign it and the theory of crisis based on it to the dustbin of history. A large part of his paper is devoted to questioning whether the LTFRP is a genuine law, whether Marx really subscribed to it in the end, whether there is good evidence that the rate of profit fell, and whether it fell for the reason the law says it tends to fall. I will respond to all this as well.

Two other aspects of Harvey’s paper will also be discussed:

- Harvey claims that the growth of the global labour force since the 1980s suggests that the LTFRP has not been operative. I will show that this claim is based on an elementary misunderstanding of the law.

- Harvey claims that Marx argued that ‘if wages are too low[,] then lack of effective demand will pose a problem’. I will show that this contradicts his own recent interpretation of Marx’s text, (Harvey 2012) and argue that he got it right the first time.

Let me note that his attitude to the LTFRP is neither surprising nor unique. Although he writes that the theory of crisis based on Marx’s law ‘holds an iconic position within the Marxist imaginary’, in fact nothing has been more reviled. In academia as well as the political realm, other Marxists and leftists have regularly denounced the supposed dogmatism of the theory and its supporters, and they have tried to exclude the theory from further consideration. For example, in their History of Marxian Economics, professors M. C. Howard and J. E. King (1992, p. xiii) wrote that the LTFRP ‘has done much damage to the intellectual credentials of Marxian political economy’, while Kshama Sawant’s organisation, Committee for a Workers’ International, recently suspended two ‘dogmatists’ from membership. It is particularly objectionable that efforts to exclude a potential explanation from consideration are presented as opposition to dogmatism, and that this spin is so often accepted.

The labour force data

Harvey cites a statistic which suggests that employment has increased markedly—the global labour force increased by 1.1 billion workers between 1980 and 2005—and he tries to use this as evidence against the idea that the global rate of profit has fallen. He devotes more than a thousand words to the topic, arriving at the conclusion that

those who attribute the difficulties of contemporary capitalism to the tendency of the profit rate to fall are, judging by this evidence of labour participation, seriously mistaken. The conditions point to a vast increase and not a constriction in surplus value production and extraction.

The data do indeed suggest that the mass—the absolute amount—of surplus-value or profit increased. But the issue here is what happened to the rate of profit, the amount of surplus-value or profit as a percentage of the volume of invested capital. An increase in the numerator of a ratio (rate) is not evidence that the ratio as a whole has increased. If the percentage increase in the denominator of the rate of profit, the invested capital, was greater than the percentage increase in the numerator, then the rate of profit fell. Given that Harvey does not show, and does not even suggest, that the denominator failed to increase by a greater percentage, the statistic he cites is just not evidence that the rate of profit rose.

However, Harvey contends that the increase in employment is, by itself––irrespective of any increase in invested capital––crucial evidence that Marx’s LTFRP has not been operative since the early 1980s. ‘If the general theory of the tendency for profit rates to fall is correct, then the spread of labour-saving technological changes … should mean a tendency for the number of waged workers employed by capital to decrease. This was something that Marx himself freely acknowledged’.

This is simply incorrect. The passage that Harvey cites in support of his claim that Marx ‘freely acknowledged’ that the LTFRP implies declining employment actually says that labour-saving technical change (‘the development of productivity’) ‘reduces the total quantity of labour applied by a given capital’. (Marx 1991a, pp. 355–56; emphasis added) ‘Applied by a given capital’ means ‘applied by a capital of given size’. If, for example, the invested capital is originally $1 million and 10 workers are employed, while later the invested capital is $4 million and 20 workers are employed, the number of workers employed ‘by a given capital’—e.g., per million dollars of capital—has fallen from 10 workers to 5. This does not mean what Harvey takes it to mean, namely that the absolute volume of employment has fallen. The absolute volume of employment has doubled, from 10 workers to 20.

Furthermore, in an extended discussion near the start of his presentation of the LTFRP, Marx explicitly denied what Harvey says he ‘freely acknowledged’:

The law of a progressive fall in the rate of profit … in no way prevents the absolute mass of labour set in motion and exploited by the social capital from growing, and with it the absolute mass of surplus labour it appropriates …

The fall in the rate of profit does not arise from an absolute decline in the variable component of the total capital but simply from a relative decline, from its decrease in comparison with the constant component.

… The absolute magnitude of profit, its total mass, would thus have grown by 50 per cent, despite the enormous decline in the general rate of profit. The number of workers employed by capital, i.e., the absolute mass of labour it sets in motion, and hence the absolute mass of surplus labour it absorbs, the mass of surplus-value it produces, and the absolute mass of profit it produces, can therefore grow, and progressively so, despite the progressive fall in the rate of profit. This not only can but must be the case—discounting transient fluctuations — on the basis of capitalist production. (Marx 1991a, pp. 322–24; emphases in original)

One would be hard pressed to put the point more definitively and emphatically. A rise in employment is just not evidence against the LTFRP.

Marx’s ‘apparent vacillation and ambivalence’

In an effort to justify his ‘long-standing skepticism about the general relevance of the law’, Harvey writes, ‘We know that Marx’s language increasingly vacillated between calling his finding a law, a law of a tendency or even on occasion just a tendency’. Yet what Harvey construes as vacillation between ‘tendency’ and ‘law’ is in fact an unavoidable distinction between what occurs in the world and what explains why it occurs. Marx noted that the rate of profit has a tendency to fall, and he put forward a law to explain why it tends to fall. Where is the vacillation?1

Nor did Marx vacillate between calling the LTFRP a ‘law’ and calling it a ‘law of a tendency’; he regarded all economic laws as laws of tendencies. In chapter 10 of volume 3 of Capital, for instance, he wrote, ‘We assume a general rate of surplus-value of this kind, as a tendency, like all economic laws …’. (Marx 1991a, p. 275) The point is simple enough: one cannot identify a law that accounts for every fluctuation in an economic variable like the rate of profit, because these fluctuations are not purely law-governed. They are affected by all manner of contingencies and impediments. One can only identify laws of the tendencies the variable exhibits amid and despite the contingencies and impediments.

Yet Harvey has additional grounds for his belief that Marx was ambivalent about the LTFRP. For one thing, ‘Marx made no mention of any tendency of the rate of profit to fall in his political writings such as The Civil War in France’. The Civil War in France also makes no mention of any phenomena such as surplus labour and surplus-value. Would Harvey regard this absence as legitimate evidence that Marx had doubts about the existence of surplus labour or surplus-value? Would he regard it as justification for ‘long-standing skepticism about the[ir] general relevance’?

As further evidence of Marx’s supposed doubts about the LTFRP, Harvey notes that his analyses of the crises of 1848 and 1857 depict them as ‘commercial and financial crises’ and refer to the falling rate of profit only in passing. Michael Krätke, a Marx-scholar, has made a similar argument. This may seem like important evidence to those accustomed to now-prevalent Marxist terminology, in which recessions and depressions are called crises, but word usage has shifted a good deal since Marx’s time. When he referred to economic crises, he meant commercial and financial crises. He distinguished these crises from the economic downturns they trigger, characterising the successive phases of the business cycle as ‘periods of moderate activity, prosperity, over-production, crisis and stagnation’, and ‘periods of average activity, production at high pressure, crisis, and stagnation’. (Marx 1990, pp. 580, 785)

Moreover, Marx did not regard the tendency of the rate of profit to fall as an immediate cause of commercial or financial crises. He argued that a decline in the rate of profit leads to a crisis indirectly and after some delay. It promotes overproduction (by, e.g., depressing productive investment demand). It also promotes financial speculation and swindling: ‘If the rate of profit falls … we have swindling and general promotion of swindling, through desperate attempts in the way of new methods of production, new capital investments and new adventures, to secure some kind of extra profit’. It is only when debts finally cannot be repaid that a crisis––that is, a financial crisis––erupts, and the crisis then leads to stagnation: ‘The chain of payment obligations at specific dates is broken in a hundred places, and this is still further intensified by an accompanying breakdown of the credit system, which had developed alongside capital. All this therefore leads to violent and acute crises, sudden forcible devaluations, an actual stagnation and disruption in the reproduction process, and hence to an actual decline in reproduction’. (Marx 1991a, pp. 349–50, 367, 363)

Once we understand that Marx was referring to ruptures of commercial and financial relations when he used the term ‘crisis’, and that he recognised the existence of many intermediate links between the fall in the rate of profit and the outbreak of crisis, it is neither surprising nor particularly significant that he sometimes discussed crises in abstraction from the tendency of the rate of profit to fall. He was just being rigorous and dialectical, dealing with one thing at a time rather than creating a chaotic jumble by dealing with everything at once.

Harvey also remarks that ‘Marx never went back to the falling rate of profit theory’ after 1868 and that ‘it does seem passing strange that Marx would chose to ignore in the last dozen years of his research what he had earlier dubbed in the Grundrisse as “the most important law of political economy”’. However, the inference that Marx ‘ignore[d]’ the LTFRP does not follow from the evidence. When I have resolved a theoretical or empirical question to my satisfaction, I don’t continue to dwell on it obsessively, but move on. That doesn’t mean that I ignore the answer I arrived at; I take it as given. The evidence suggests to me that Marx worked in a similar way. In what way does Harvey work?

So the real question is whether, before moving on, Marx was satisfied with his explanation of why the rate of profit tends to fall. The evidence leaves little room for doubt. In response to Michael Heinrich (who recently made arguments similar to Harvey’s), my co-authors and I presented ‘considerable evidence in Marx’s correspondence – spanning the period from 1865 to 1877 – that he was satisfied with his theoretical results and that he regarded Capital, not only the first volume that he published but also the volumes that remained unpublished, as a finished product in a theoretical sense’ (Kliman, Freeman, Potts, Gusev, and Cooney 2013) Heinrich has not responded to this evidence, and Harvey refrains from discussing it.

As for Marx’s view that the LTFRP was the most important law of political economy, this was not a one-off comment made early on and then ‘ignored’. He affirmed this not only in the 1857-58 Grundrisse, but also in his 1861–63 economic manuscript: ‘This law, and it is the most important law of political economy, is that the rate of profit has a tendency to fall with the progress of capitalist production’. (Marx 1991b, p. 104; emphasis in original) Later, when writing volume 3 of Capital, Marx went beyond the claim that the LTFRP was the most important law. He now contended that it was so important that all of political economy since Adam Smith had revolved around a search for this law: ‘given the great importance that this law has for capitalist production, one might well say that it forms the mystery around whose solution the whole of political economy since Adam Smith revolves’. (Marx 1991a, p. 319)

The mythical mono-causal theory

Harvey’s inadequate understanding of Marx’s text is also what lies at the root of his charge that the LTFRP and theory of capitalist crisis rooted in it are mono-causal. He contends that Marx’s law is derived from a ‘highly simplified model[ ]’ that rests on a number of ‘draconian’ assumptions. That is, the law is valid only if all of the assumptions hold true in the real world. But by virtue of these assumptions, the law excludes all potential causes of falling profitability other than labour-saving technical change, and it excludes all factors that can keep the rate of profit from falling by counteracting the effect of technical change. Thus the law is mono-causal , as is any theory of crisis that employs it without combining it eclectically with extraneous factors.

Yet Harvey acknowledges that the draconian assumptions are not to be found in Marx’s text: ‘While Marx scrupulously lays out his assumptions in Volume 1 [of Capital] he does not do so in the case of the falling rate of profit theory [in Volume 3]’. How, then, does he know that Marx actually made these draconian assumptions?

In one case, at least, he is demonstrably wrong. According to Harvey, Marx’s law assumes that all commodities (‘with the exception of labour power’) are bought and sold at their actual values, rather than at prices which differ from these values.2 That is just not the case. The law is the subject of Part 3 of the third volume. Marx has already, in Part 2, derived the result that, however large the discrepancies may be between commodities’ values and the prices at which they actually sell, the total price of output in the economy as a whole is equal to (and thus limited by) the total value of this output. Consequently, when the price that one firm or industry receives for its product exceeds the product’s value, this gain comes purely at the expense of an offsetting loss incurred by other capitalists. The prices of their products are less than their values. And it follows from this, first, that total profit is equal to (and limited by) the total surplus-value that has been created, and second, that discrepancies between prices and values leave unaffected the economy-wide rate of profit to which the LTFRP pertains.3

These results, not some assumption that everything sells at its value, are the basis upon which Marx (1991b, p. 104; emphases in original) derived the law of the tendential fall in the rate of profit:

We have seen that [the rate of profit] is different for the individual capital [from] the ratio of the surplus value to the total amount of the capital advanced. But it was also shown that considering the … total capital of the capitalist class, the average rate of profit is nothing other than the total surplus value related to and calculated on this total capital …. Here, therefore, we once again stand on firm ground, where, without entering into the competition of the many capitals, we can derive the general law directly from the general nature of capital as so far developed. This law, and it is the most important law of political economy, is that the rate of profit has a tendency to fall with the progress of capitalist production.

In general, Harvey turns Marx’s law into a model that depends on a host of restrictive assumptions by construing the law as narrowly as possible. He does not regard the whole of Part 3 of the third volume, but only the material dealing with what Marx called ‘the law as such’ (das Gesetz als solches), as a presentation of the law. This makes the law seem mono-causal and disconnected from other phenomena and institutions that Marx discusses later in Part 3. It seems not to be a law that operates amid various counteracting factors and through the intermediation of the financial system (as I discussed above), but an other-worldly abstraction that can be called a law only under imaginary conditions that exclude and ignore so much that matters in the real world.

Harvey says that Marx’s ‘exclusion[ ]’ of so much ‘severely restricts [the law’s] applicability’. Although he knows that Marx went on to introduce other phenomena and institutions into the analysis, his cordoning off of ‘the law as such’ prevents him from recognising this as evidence of the multi-causal character of the LTFRP. The introduction of additional phenomena and institutions into the analysis no longer seems to be a dialectical enrichment of the law that describes it in the concrete forms in which it manifests itself, but a tacit admission that the conditions which need to be present in order for the law to operate are not in fact present. The law seems not to ‘remain[ ] intact’. Marx seems to be engaged in a separate discussion from before, one concerned with ‘what happens when the assumptions made in deriving the law are dropped’. He seems to be calling the status of the law into question, exhibiting his ‘vacillation and ambivalence’. And we seem to be in need of a very different framework for crisis theory, an unstructured space populated by a host of potential explanatory factors and phenomena that have no intrinsic connections to one another, factors and phenomena too distinct from one another to be ‘cram[med …] into some unitary theory’.

The text need not be read in this way. And since it need not, it should not; uncharitable reading is not good interpretive practice.

No sophisticated methodological discussion is needed to understand what’s wrong with the charge of mono-causality. The issue is simple. If I appeal to the universal law of gravitation in order to explain why apples have a tendency to fall off trees, without mentioning other factors that can make them fall, like the blowing of the wind, or counteracting factors, like air resistance, I am not assuming that these other things don’t exist. Much less am I constructing a mono-causal model that excludes them and which is therefore severely restricted in applicability. I am not doing so even if I explain that the law of gravitation follows from Newton’s second law of motion and refrain from introducing other factors into the equation when I show how it follows. If I then go on to talk about air resistance and the blowing of the wind, I am not exhibiting my ambivalence, vacillating, or admitting that the universal law of gravitation operates only in a vacuum, but fails to operate in the real world.4

Harvey is correct that Marx’s law is not the ‘absolute truth’ of capitalism’s dynamics. In other words, it is not their sole cause. It does not even account for every blip in the trajectory of the rate of profit. But that is not the purpose of the law. Its purpose is ‘merely’ to show that Marx’s value theory, in conjunction with his theory of capital accumulation, can account for the fact that the rate of profit tends to fall.

For the most part, Harvey is quite vague about exactly who the modern-day objects of his criticisms may be. For example, he alleges that the crisis theory rooted in the LTFRP is ‘typically presented’ by its current proponents ‘in such a way as to exclude consideration of other possibilities’ and that ‘many Marxist economists like to assert’ that there is a ‘single causal theory of crisis’. The fact that he refrains from naming names makes it hard to answer his charges. At one point, however, he claims not only that ‘[s]ome proponents’ of the law ‘suggest … that financialisation had nothing to do with the crash of 2007–8’, but also that ‘Andrew Kliman has been most strident in his claim that the crisis had nothing to do with financialisation’. However, I do not claim this stridently. I do not even claim it while paying due deference to my superiors. I claim the opposite: ‘Of course, a financial crisis triggered the recession, and phenomena specific to the financial sector (excessive leverage, risky mortgage lending, and so on) were among its important causes’. (Kliman 2012, p. 6)

The sentence I have just quoted comes from the first chapter of my book on the underlying causes of the Great Recession.5 Part of the next chapter ‘focus[es] on two intermediate links—low profitability and the credit system—that connect the fall in the rate to profit … to the latest economic crisis and slump’. (Kliman 2012, pp. 16–17) And chapter 3, devoted to the financial crisis of 2007–8, discusses the following: the Federal Reserve’s excessively easy-money policy after the dot-com bubble of the 1990s burst; securitisation of mortgage loans; subprime lending; home-equity lines of credit; rising loan-to-value ratios for mortgage loans; lenders’ rising leverage ratios and reduced capital requirements; the rise in household debt during the 1990s and 2000s; the psychology that gave rise to the dot-com and home-price bubbles; the disastrously incorrect forecasting models of the credit-rating agencies; Congress’ initial rejection of the TARP (Troubled Assets Relief Program) bailout; and the inflow of savings from abroad that made its way into the U.S. If this is Harvey’s best example of denial that financialisation was a cause of the 2007–8 financial crisis,6 or of a mono-causal approach, I would hate to see his other examples.

References

- Harvey, David. 2012. History versus Theory: A Commentary on Marx’s Method in Capital, Historical Materialism 20:2, 3–38.

_______. 2014. Crisis Theory and the Falling Rate of Profit. - Howard, M. C. and J. E. King. 1992. A History of Marxian Economics: Volume II, 1929–1990. Princeton, NJ: Princeton Univ. Press.

- Kliman, Andrew. 2007. Reclaiming Marx’s “Capital”: A Refutation of the Myth of Inconsistency. Lanham, MD: Lexington Books.

_______. 2012. The Failure of Capitalist Production: Underlying Causes of the Great Recession. London: Pluto Books. - Kliman, Andrew, Alan Freeman, Nick Potts, Alexey Gusev, and Brendan Cooney. 2013. ‘The Unmaking of Marx’s Capital: Heinrich’s Attempt to Eliminate Marx’s Crisis Theory’.

- Kliman, Andrew and Shannon D. Williams. 2014. ‘Why “Financialisation” Hasn’t Depressed US Productive Investment’, Cambridge Journal of Economics. Print version forthcoming.

- Marx, Karl. 1990. Capital: A Critique of Political Economy, Vol. I. London: Penguin.

_______. 1991a. Capital: A Critique of Political Economy, Vol. III. London: Penguin.

_______. 1991b. Karl Marx, Frederick Engels: Collected Works, Vol. 33. New York: International Publishers.

Notes

1 See Kliman, Freeman, Potts, Gusev, and Cooney (2013) for a discussion of the law’s function and the meaning of ‘law’ in this context.

2 He contends that volume 3 of Capital retains the assumption, made throughout much of volumes 1 and 2, that ‘[a]ll commodities trade at their value (with the exception of labour power)’. However, the assumption in question does not exclude labour-power. By assuming that labour-power, too, is purchased at its full value, Marx was able to explain how profit arises in production, not the market, and to explain this without abandoning the idea that commodity exchange is ‘in fact a very Eden of the innate rights of man … the exclusive realm of Freedom, Equality, Property, and Bentham’. (Marx 1990, p. 280)

3 I am aware of the allegation that Marx’s derivation of these results has been proven to be internally inconsistent, but that is only a pernicious myth. See chap. 8 of Kliman (2007).

4 I think this analogy to Marx’s procedure holds strictly, point by point. The law of gravitation is the analogue of the LTFRP; the second law of motion is the analogue of the law of the determination of value by labour-time (‘law of value’).

5 Harvey cites my book elsewhere in his paper, but he provides no evidence or citation to support his version of what I claim.

6 Shannon Williams and I (Kliman and Williams (2014)) have shown that financialisation was not the cause of the fall in U.S. corporations’ rate of capital accumulation during the decades that preceded the Great Recession. That is of course an entirely different matter.

Part 2: Getting Profitability Wrong

The first part of this article focused on David Harvey’s interpretation (Harvey 2014) of Marx’s law of the tendential fall in the rate of profit (LTFRP) as capitalist production increases—a law Marx identified as ‘the most important law of political economy’. It remains to address Harvey’s belief that the LTFRP has not in fact been operative since the 1980s.

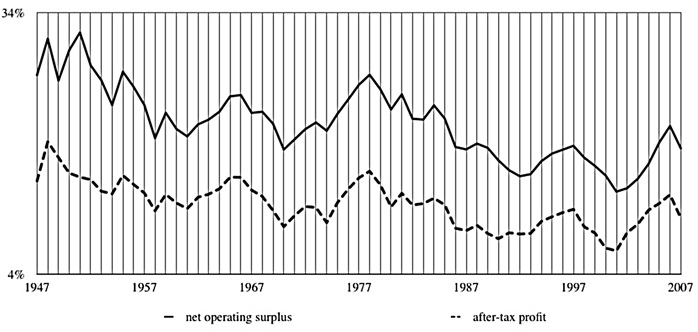

The labour-force data discussed in part 1 constitute Harvey’s only ‘evidence’ that the LTFRP has not been operative; he provides no direct evidence regarding the rate of profit (i.e. the amount of profit as a percentage of the volume of invested capital). However, he does challenge the evidence that has been put forward by myself and others which indicates that the rate of profit fell throughout the 1980s and 1990s (see Figure 1).1

Figure 1. U.S. Corporations’ Rate of Profit

Harvey says that ‘some serious questions have to be asked’ about this evidence. He is quite right, and he asks crucially important questions. The problem is that his discussion proceeds as if his questions are ones that we have never heard nor taken into account. They are actually long-standing, standard questions. I for one have taken all of them into account when gathering and interpreting my data. There is therefore no need to respond to them; my analyses and interpretations of the data have already anticipated and dealt with them. I simply need to make clear how they have done so.2

What Harvey calls his ‘most important objection’ to ‘much of the falling-rate-of-profit literature’––once again, he is vague about the object of his critique––is the fact that ‘[p]rofit rates can fall for any number of reasons’. Therefore ‘[d]ata that show a falling rate of profit do not necessarily confirm the existence of the specific mechanism to which Marx appealed’ (labour-saving technical change).

This is exactly right. Thus, when I considered the trajectory of U.S. corporations’ rate of profit from the end of World War II to the Great Recession and I concluded that ‘Marx’s law of the tendential fall in the rate of profit fits the facts remarkably well’ in this case, (Kliman 2012, p. 137) my conclusion was not based on the mere fact that the corporations’ rate of profit fell. It was based on a ‘decomposition analysis’ that separates out (decomposes) various potential causes of the fall and measures the effect that each one had on the rate of profit. Moreover, because the standard way of decomposing the rate of profit is not particularly appropriate when conducting a causal analysis (for a reason stressed by Harvey), I decomposed it in a different manner.

Traditionally, the rate of profit has been decomposed into the rate of surplus-value (or ratio of profit to employee compensation) and a function of the value composition of capital (or ratio of the constant to the variable components of the capital-value advanced (invested)). This is fine in some contexts, but the nominal value composition of capital that researchers construct is different from the value composition to which Marx refers. It is affected not only by the relative amounts of value invested to acquire means of production and hire workers, but also by changes in the rate at which commodities’ money prices rise in relation to the commodities’ actual values. Because two different factors affect it, movements in the nominal value composition have no clear-cut, unambiguous meaning. For example, when the nominal value composition remains constant, as it did in the U.S. during the 1960s and 1970s, we cannot conclude that the relative amounts of value invested to acquire means of production and hire workers also remained constant. It is possible that relatively more value went to acquire means of production, which tends to raise the value composition, but that this effect was offset by accelerating inflation.3 As Harvey correctly emphasises, this is a ‘major problem’.

My alternative decomposition dealt with this problem by separating the two determinants. I decomposed the overall movements in the rate of profit into

- movements caused by changes in the rate at which commodities’ money prices rise in relation to the commodities’ actual values;

- movements caused by changes in the ratio of profit to employee compensation, and

- movements caused by ‘everything else’.

I found that, although the first two causes had been important during certain shorter periods, neither of them had a substantial effect on the rate of profit in the long term—that is, when we consider the postwar era as a whole. Almost the entire long-term fall in the rate of profit was therefore caused by changes in ‘everything else’.

But once (1) and (2) have been set aside, it follows mathematically that ‘everything else’ is just the ratio of employment to the amount of capital invested in fixed assets, as measured in terms of labour time. Almost all of the long-term fall in the rate of profit is attributable to the decline in this ratio. In other words, it is attributable to the fact that employment consistently grew less rapidly than capital accumulated. This is precisely how Marx’s law explains the long-term tendency of the rate of profit to fall. Thus, the law accounts for almost all of the fall in U.S. corporations’ rate of profit.

The ratio of profit to employee compensation had little effect on the rate of profit because it changed very little. (It fell a bit during the early part of the postwar period, but had no upward or downward trend between 1970 and the Great Recession.) It is important to emphasise that the long-term stability of this ratio is not a statistical mirage caused by the fact that the U.S. government classifies the pay of CEOs and other top corporate executives as employee compensation rather than as profit. Recent estimates of mine (see Kliman 2014b) indicate that re-classification of top executives’ pay as profit makes very little difference. Yes, their pay skyrocketed in recent decades, but there were simply too few top executives for this to have had much effect on the numbers. Between 1979 and 2005, the rising share of the product received by managers in ‘the 0.1%’ and ‘the 1%’ (the top 0.1 percent and top 1 percent of the income distribution) depressed other business-sector employees’ share by only 0.4 and 0.6 percentage points, respectively, according to my estimates.

Another of Harvey’s objections to the falling-rate-of-profit evidence is that ‘[t]here is a gap between where profit (value [sic]) is produced and where it may be realised. … The patterns of … flows of capital and revenues are intricate and it is not clear that data collected at one point in the system accurately represent the movements in their totality’. He is correct once again. It would be wrong to conclude from the data discussed above––which pertain to the profitability of domestic capital investment––that there was a decline in U.S. corporations’ overall rate of profit, on foreign as well as domestic investment. My conclusion that the rate of profit fell was instead based upon consideration of both the foreign and the domestic accounts. Government data on U.S. corporations’ capital investments abroad and their profits from investment abroad are available from the start of 1983 onward. They indicate clearly that U.S. multinational corporations’ rate of profit on foreign investment trended downward substantially between the start of this period and the Great Recession (see Figure 2)4. Because the denominators of the domestic and foreign rates of profit measure somewhat different things, the two data sets cannot properly be combined, and thus we cannot ascertain the exact extent to which U.S. corporations’ overall rate of profit fell. However, the fact that both the foreign and domestic rates of profit declined does mean that we can be confident that the overall rate of profit did indeed fall.

Figure 2. U.S. Multinational Corporations’ Rate of Profit Abroad

(after-tax income from foreign direct investment as a percentage of accumulated foreign direct investment)

Harvey also notes correctly that U.S. multinationals use ‘transfer pricing’ to shift profits generated in one country onto the books of a subsidiary in a different country where they are not taxed or are taxed at a lower rate. He could have added the fact that multinationals’ foreign profit and investment data are attributed to the countries in which their foreign subsidiaries are incorporated, which frequently differ from the countries where production takes place and the products are sold. As a result, it is difficult if not impossible to know what the multinationals’ rate of profit in any particular country really was. But this does not matter insofar as the total picture is concerned. Transfer pricing schemes allow corporations to shift around profits and titles to investments, but they do not affect the total volume of profit or investment. Harvey claims that transfer pricing allows profits to be ‘disguise[d]’, but he provides no evidence and I know of no such evidence. Shielding profits from the reach of tax authorities is not the same thing as disguising them.

The evidence discussed above pertains to U.S. corporations only. Harvey objects that ‘it cannot be taken as evidence of what is happening to global capital’. Indeed it cannot, but what makes this fact a legitimate objection in this context? The topic of his paper is the fall in the rate of profit as a potential cause of economic crisis, and he is well aware that the latest crisis began in the U.S. before it spread throughout the world ‘through contagions in a global financial system’. Since the U.S. was the epicentre of the crisis, and its subsequent spread elsewhere has a straightforward financial explanation, what we need to focus on is whether and how a fall in the U.S. rate of profit, not the global rate, was an underlying cause of the crisis.

Harvey notes that profitability has rebounded substantially in recent years. Of course, post-recession trends have no bearing on whether a prior fall in the rate of profit was among the causes of the Great Recession. His point is rather that, since a measure of the rate of profit which fails to capture the post-recession rebound is suspect, what that measure tells us about a prior decline in profitability is suspect as well. I could not agree more, but all of the rates of profit I have computed (using more or less inclusive definitions of profit) do indeed capture the post-recession rebound. They all fell during the Great Recession—bottoming out 24 percent to 38 percent below their peak values of 2006––but by 2013, all of them had rebounded to levels close to or greater than those of 2006. The main cause of the rebound in profitability has been a sharp post-recession decline in workers’ share of the product, which in turn has been caused by companies producing more without increasing their workforces. It has not been caused by ‘wage repression’. Even after adjustment for inflation, employees’ hourly compensation has risen.

Right the first time (on Marx’s ‘underconsumptionism’)

Why does Harvey repeatedly stress that there are ‘conflicting forces’ and ‘multiple contradictions and crisis tendencies’? Why are we presented with the mono-causal LTFRP strawman? Notice what these two things imply when we take them together: since the law can hold true only if other causes of crisis and counteracting factors are assumed not to exist, we must jettison the law once we recognise that they do exist. Thus, as I noted in part 1, I suspect the talk of multi-causality is masking Harvey’s desire for an apousa-causal crisis theory. He is clearly not happy with the specific multi-causal theory of crisis that emerges, when all is said and done, from volume 3 of Capital––a theory in which the LTFRP remains intact and other determinants such as the financial system are linked to it and mediate the way in which it appears.

In particular, Harvey seems to want to impute to Marx an underconsumptionist theory of crisis––that is, a theory in which the lack of ‘effective demand’ is not the mediated result of the operation of the LTFRP and intermediate links such as businesses’ investment decisions and financial disturbances, but an independent, unrelated phenomenon produced by the masses’ restricted consumption. He attributes to Marx the notion that ‘if wages are too low[,] then lack of effective demand will pose a problem’. As evidence, he quotes a sentence in volume 3 of Capital (and a similar footnote in volume 2) in which Marx states that ‘the ultimate reason for all real crises always remains the poverty and restricted consumption of the masses’. (Marx 1991a, p. 615)

In the time-honoured fashion of underconsumptionists everywhere, Harvey strips away the context in which this sentence appears. When read in context, the sentence has nothing to do with periods in which low wages supposedly lead to inadequate demand, nor does the masses’ restricted consumption seem to be a ‘cause’ of crises in the modern sense of the word ‘cause’ (which Aristotle called ‘efficient cause’). It is merely the condition that makes crises possible (an Aristotelian ‘formal cause’), not something that turns this possibility into a reality.5

Only a few years ago, Harvey had a much clearer understanding of the sentence and the passage in which it appears, and he took care to analyse it in context. After asking where the extra demand comes from that enables the surplus-value that has been produced to be realised in money form, Harvey (2012, p. 25) noted that ‘Marx’s answer is as surprising as it is ruthlessly honest. In a two-class closed society comprised of capitalists and labourers, there can be only one source of the extra demand and that is from capital, since exploited labour could never furnish it’. In other words, it is capitalist firms’ demand for additional means of production––investment demand––and capitalist households’ demand for consumer goods that allows the portion of output that contains the surplus-value to be sold. Harvey then quoted from and summarised much of the passage in question, in order to make clear that the shortfall in demand that characterises economic crises is not due to the restricted consumption of ‘the masses’ or ‘exploited labour’, since their consumption is always restricted––crisis or no crisis. Thus, blaming the crisis on the masses’ restricted consumption is like blaming an airplane crash on gravity (which always exists, crash or no crash).

The shortfall in demand is instead caused by the fact that the extra demand that needs to come ‘from capital’ has temporarily stopped coming from capital. The key problem is that capitalism requires what Harvey (2012, p. 26) calls ‘continuous capital-accumulation’, i.e. additional investment in production, but a shortfall in demand occurs when and because the volume of additional productive investment is less than what is needed.

Since Harvey knows (or at least used to know) all this, why has he suddenly taken the ‘restricted consumption’ sentence out of context and pressed it into the service of an underconsumptionist ‘wage repression’ theory of crisis that is alien to Marx’s actual and ‘ruthlessly honest’ account of the demand problem? Perhaps the answer is that the ‘ruthlessly honest’ account takes us straight back to the fall in the rate of profit. Once we understand that a lack of demand is almost always a matter of inadequate investment demand, we are led to ask why investment is inadequate, and this question leads to two further ones: Has the volume of profit (surplus-value) that has been generated large enough to fund an adequate level of investment demand? And is the expected rate of profit on the new investments of today high enough to bring forth investment in the volume that is needed?

Inadequate profitability was a main cause of the long-term slowdown in U.S. corporations’ investment demand for productive fixed assets. Between 1948 and 2007, their rate of accumulation of fixed assets fell by 41%, while their after-tax rate of profit on fixed-asset investment fell by 43%. The only other factor that can influence the rate of accumulation is the share of profits that is re-invested in production; it actually rose a bit (3%). The entire decline in the rate of productive capital accumulation is therefore attributable to the decline in the rate of profit (see Kliman and Williams 2014 for further discussion).

Expectations that the future profitability of productive investment will be inadequate also seems to have been a major problem for some time now, as well as a crucial determinant of why recovery from the Great Recession has taken so long and has been so weak. In order to explain the feebleness of the recovery, mainstream economists and economics writers such as Paul Krugman, Martin Wolf, and former U.S. Treasury Secretary Lawrence Summers suggest that the U.S. economy entered a period of ‘secular stagnation’ some time before the recession, perhaps as early as the mid-1980s—that is, a period in which adequate demand is no longer sustainable unless real (i.e., inflation-adjusted) short-term interest rates are ridiculously low, maybe as low as –2% or –3%. This means that borrowers pay back less than they borrowed, once inflation is taken into account. If the only way to induce companies to undertake sufficient investment is to provide them with money that they don’t have to pay back, the expected rate of profit on new investments must be terribly low indeed! (See Kliman 2014a for further discussion.)

I am not ‘proclaiming that it is all a consequence of some hidden tendency for the rate of profit to fall’, as Harvey puts it. That would be wrong for two reasons. First, all manner of intermediate links and complicating factors have also been at work. (The Great Recession has also weakened businesses’ confidence in the future, to take just one example.) Second, the tendency for the rate of profit to fall is not ‘hidden’. As Hegel said, essence must appear, or shine forth, in the observable world. I think it has done so.

References

- Harvey, David. 2012. History versus Theory: A Commentary on Marx’s Method in Capital, Historical Materialism 20:2, 3–38.

_______. 2014. Crisis Theory and the Falling Rate of Profit. - Kliman, Andrew. 2012. The Failure of Capitalist Production: Underlying Causes of the Great Recession. London: Pluto Books.

_______. 2014a. Clarifying “Secular Stagnation” and the Great Recession, New Left Project. March 3.

_______. 2014b. Were Top Corporate Executives Really Hogging Workers’ Wages?, Truthdig. Sept. 18. - Kliman, Andrew and Shannon D. Williams. 2014. Why “Financialisation” Hasn’t Depressed US Productive Investment, Cambridge Journal of Economics. Print version forthcoming.

- Marx, Karl. 1991a. Capital: A Critique of Political Economy, Vol. III. London: Penguin.

Notes

1 The data used to construct Figure 1 come from the U.S. Bureau of Economic Analysis: National Income and Products Accounts Table 1.14, lines 1, 4, 7, 9, 10, and 12; Fixed Asset Table 6.3, line 2; and Fixed Asset Table 6.6, line 2. Net operating surplus and after-tax profit are measures of profit. The denominator of both rates is accumulated investment in fixed assets, net of depreciation. Depreciation is valued at historical cost.

2 I shall limit these remarks to a discussion of my own analyses, since I am less knowledgeable about others’.

3 As Harvey notes, even the ‘real’ value composition of capital––the one to which Marx refers rather than the nominal one––is not purely an index of labour-saving technical change. In this respect, it differs from the ‘technical’ and ‘organic’ compositions. However, my estimates indicate that U.S. corporations’ real value composition tracked the technical and organic compositions quite closely. Between 1947 and 2007, the real value composition increased by about 120% while the technical and organic compositions increased by about 160%. Throughout almost all of this period, the relation between the different compositions of capital was even stronger than these numbers suggest. The difference in growth rates is largely due to brief periods (the latter parts of the 1960s and 1990s) in which exceptionally rapid wage growth temporarily depressed the real value composition.

4 The data used to construct Figure 2 come from the U.S. Bureau of Economic Analysis’ ‘Balance of payments and direct investment position data’ tables. The numerator of the rate of profit is ‘Direct Investment Income Without Current-Cost Adjustment’; the denominator is ‘U.S. Direct Investment Position Abroad on a Historical-Cost Basis’. The data are for ‘all countries’.

5 For further analysis of the passage, see pp. 165–67 of Kliman (2012). For discussion of the logical and empirical flaws of the underconsumptionist theory of crisis, see chap. 8 of the book.

1 Trackback / Pingback