[MHI Note: This article originally appeared in New Left Project on May 19, 2014. Republished with permission.]

by Andrew Kliman

In my initial response to Sam Gindin, I noted that “his broad-brush, holistic account of the ‘neoliberal’ period is not sensitive enough to the details of the data.” Unfortunately his reply suffers from the same problem. It has a strong narrative line and it marshals evidence, but it lacks sufficient concern for the need to analyse the evidence and understand its implications. Using evidence to give one’s story verisimilitude is not enough. I shall focus on this issue in my rejoinder; foregoing the opportunity to comment on other questionable aspects of Gindin’s reply, in the hope that the discussion can then proceed on the basis of a shared understanding that theory needs to be grounded in careful consideration of evidence.

Secular Stagnation

The economy remains stuck in a state of near-stagnation and secular (long-term) stagnation remains a distinct possibility. Yet the financial crisis in the U.S. was resolved five or more years ago. It therefore seems implausible to many observers, including Paul Krugman, Lawrence Summers, Robin Wells, Martin Wolf, and myself, that the financial crisis was the fundamental cause of the Great Recession and the continuing malaise. How could they be mere effects of a problem that was resolved so long ago? Despite this, Sam Gindin remains adamant that “the cause of our economic malaise was [not something] more fundamental than a mere crisis in finance.” Yet he fails to provide a prosaic economic cause-and-effect linkage.

When David Ricardo was unable to find a prosaic economic explanation for the tendency of the rate of profit to fall, he “fle[d] from economics to seek refuge in organic chemistry,” as Karl Marx put it. Gindin does something similar, fleeing from economics to seek refuge in abnormal psychology: “This was an especially traumatic crisis, and it understandably left consumers and investors hesitant to spend.” But corporations don’t suffer from post-traumatic stress disorder. They aren’t even people, really. The idea that their investment decisions are driven by nightmares and flashbacks to the fall of 2008, rather than by statistical projections provided by the armies of paid professionals they employ—statistical projections of future profitability––is not plausible. Gindin underestimates them.

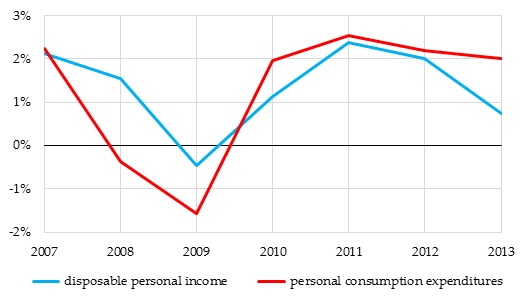

Furthermore, the idea that consumers have been hesitant to spend their income because they remain traumatized is inconsistent with the evidence. As Figure 1 shows, consumption spending in the U.S. increased as rapidly, or more rapidly, than disposable (i.e., after-tax) income in each of the last four years. After adjustment for inflation, disposable income rose by a total of 6.4% between 2009 and 2013 while consumption rose by 9.0%. Spending on new home construction, which is not included in the consumption spending figures, rose even more sharply. Between the final quarters of 2010 and 2013, it increased by 30.4% in inflation-adjusted terms.[1] Thus, the needed cause-and-effect linkage between the financial crisis and the current economic malaise is still lacking.

Figure 1. Personal Consumption and After-Tax Income, U.S. (inflation-adjusted annual growth rates)

The Size of “the Stimulus”

My initial response to Gindin noted that economic malaise persists in the U.S. even though its fiscal policy (as well as its monetary policy) has been wildly expansionary. The public debt has risen by 89% since the start of 2008. The additional borrowing, $8.2 trillion, has been used to fund increased federal government spending and lower federal taxes. Despite this, Gindin insists that “the federal stimulus was significantly offset by cutbacks at state and local levels—the net two year stimulus was therefore about one third of the $780 billion in the American Recovery and Reinvestment Act” (ARRA). Yes, but when he refers to “the federal stimulus,” he is only talking about the ARRA. I am talking about the entire stimulus, which to date amounts to $8.2 trillion dollars, even though only a small part of that stimulus was officially christened as “the stimulus.” The entirety of the extra spending and reduced taxes is stimulative––expansionary fiscal policy––and this is the case even though much of the $8.2 trillion of stimulus consists of automatic stabilizers instead of changes in spending and tax law (see the Tax Policy Center’s “Economic Stimulus: How do automatic stabilizers work?” webpage).

If we’re talking about the entire stimulus, not just the ARRA, it cannot be said that state and local government cutbacks have offset the federal stimulus. State and local government deficits (which likewise fund increased government spending and tax reductions) have increased markedly since the Great Recession. In 2007, the total state and local deficit was $73 billion. It rose to $165 billion in 2008, and it averaged $239 billion per year between 2009 and 2013.[2]

Gindin suggests that “radically greater economic stimulus” would bring about a solid economic recovery. But how much greater is “radically greater,” and is this a feasible proposal? Let’s assume that solid recovery would require additional government stimulus three to five times as large as the stimulus to date. Were it actually the case that the stimulus during the last six and a half years amounted to a measly one-third of the $780 billion allocated to the ARRA, then additional stimulus of about $800 billion to $1300 billion would suffice. That is a reasonable amount of new borrowing, so the government’s failure to borrow that sum and extricate the economy from its malaise could be blamed on greedy financial interests who benefit from austerity and largely dictate the direction of government economic policy, as Gindin argued in his initial article. One wouldn’t have to face up to the deep structural problems that pre-date the financial crisis and that continue to hamper economic recovery. Nor would one have to face the fact that “Keynesian” policies––the panacea proposed by the anti-austerity wing of capital and its allies to the left––have already been tried in a big way in the U.S., and they have been found wanting.

But the true size of the federal, state, and local government stimulus has thus far been about $9.5 trillion. What would another $800 billion or $1300 billion do? Even if the “radically greater economic stimulus” a solid recovery requires is only twice as large as the stimulus to date, new government borrowing of about $19 trillion is needed.

Yet it is important to bear in mind that artificial stimulus has only a temporary effect. Once the increase in borrowing goes into reverse, so does the stimulus it provided. This is not highfalutin Marxian theory. It is what Keynesian economics itself says. Yes, there is the famous Keynesian multiplier effect––extra government spending and tax cuts boost income, which boosts spending again, which boosts income again, and so on. But those who think that the multiplier effect implies that artificial stimulus sets in motion a perpetual economic-growth machine simply haven’t understood the basics of Keynesian theory.

Thus, to bring about solid recovery in the face of a secular-stagnation tendency, really radical economic stimulus might be needed for a very long time. Government debt might well have to rise by 30, 40, 50 or trillion dollars, perhaps more. As I think even Gindin would agree, such a huge increase in borrowing would cause interest rates to rise to stratospheric and catastrophic levels. Once one understands this, one has to face up to the structural problems and the limited efficacy of artificial stimulus.

The Fall in the Rate of Profit

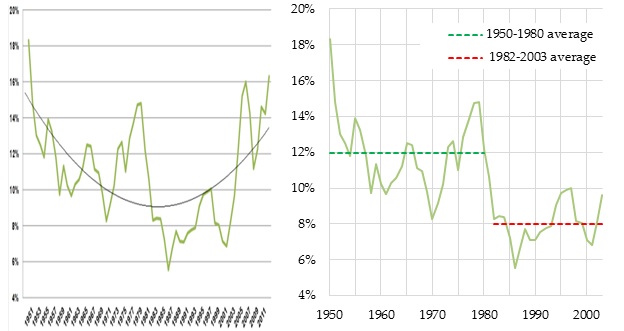

Gindin asserts that there was no “protracted crisis of profitability” during the quarter-century preceding the Great Recession. On the contrary, “it has been [sic!] one of the most dynamic eras for capital in American history.” To support this assertion, he provides graphs that purportedly show that U.S. corporations’ after-tax rate of profit, and their profits as a share of GDP, rebounded smartly after the early-1980s. He concludes triumphantly that “Kliman cannot reverse the weight of evidence stacked against him.”

But there is no evidence to reverse. Gindin’s own evidence contradicts his narrative. The left panel of Figure 2 is Gindin’s rate-of-profit graph; the right panel is the same rate of profit for the period between 1950 and 2003.[3] The after-tax rate of profit, which was 14.8% in 1979, fell to 12.2% in 1980. That was just a tad above the 12.0% average rate of profit during the preceding three decades.

Figure 2. Gindin’s After-Tax Rate of Profit, U.S. Corporations, 1950-2012 and 1950-2003

The rate of profit continued to fall. In 1982 it was 8.3%. And even though 1982 was a year of deep recession, the average rate of profit during the next 21 years was even lower, 8.0%. Gindin’s rate of profit did not return to its 1980 level until 2004, the middle of the phony “boom” created by the home-price bubble that burst a few years later. It is also clear that, contrary to what Gindin claims, the downward slide in profitability that began at the end of the 1970s did not end once the economy pulled out of the recession of the early 1980s. The rate of profit continued to fall through 1986, the second year of Ronald Reagan’s second term as U.S. President.

Gindin seems to have been misled by his smiley-face trend curve, which virtually cries out “Have a Nice Neoliberal Recovery.” But don’t let its glad expression give you the wrong impression. Gindin’s own figures indicate clearly that profitability did not recover until the phony “boom” that triggered the crash.[4]

In my initial response to Gindin, I noted that

When economists such as Summers and Krugman hypothesize that the ‘natural’ real short-term interest rate had become negative well before the financial crisis, what they mean is that the expected profitability of investment in production had fallen to such a low level that something approaching full employment was no longer sustainable given normal interest rates.

Gindin disputes this. He maintains that mainstream economists’ concern over the prospect of secular stagnation is based, not on a “lack of profits” but “the lack of investment from the obviously high profits.” As evidence, he quotes Krugman’s statement that “from a profits point of view it’s not a depressed economy at all,” but he fails to mention that Krugman was referring only to the period since the Great Recession began. Krugman’s very next sentence was “Look at profits versus compensation of employees (that’s wages and benefits combined) since the slump began at the end of 2007 ….” (emphasis added). Thus, the quotation is irrelevant here, where the issue is the level of the “natural” real short-term interest rate “before the financial crisis” (emphasis added). I maintain that Krugman, Summers, et al. are saying in effect that low expected profitability—prior to the financial crisis—had made a normal volume of productive investment impossible unless interest rates were exceptionally low. If Gindin wants to challenge my interpretation, he needs to show that these economists’ theory of investment behaviour is not one in which productive investment depends principally on the relation between expected profitability and interest rates. I don’t think he will succeed.

Working-class Income

My initial response to Gindin showed that the income and pay of the working class as a whole did not stagnate under “neoliberalism,” contrary to popular belief on the left. When income is defined in a comprehensive manner, each of the bottom three quintiles (20% groups) of U.S. households experienced a rise in income of more than 30% between 1979 and 2007, and inequality went into reverse after 1989. During the same 28-year period, median wages of women rose by 34% while median earnings of workers employed full-time, year-round, rose by 22%. These wage figures exclude employer-provided benefits, which rose even more rapidly (as Gindin concedes). As shares of net output, compensation of employees did not fall, and profit and other business income did not rise, between 1970 and the Great Recession, either in the U.S. corporate sector or in the business sector as a whole. And when we add in net government social benefits, working-class income trended upward slightly as a share of net output.

Gindin does not challenge any of this evidence. What he actually does, in his haste to reassert his story that the working class suffered a massive defeat under neoliberalism, is disregard evidence, dismiss it, and deal cavalierly with it.

Workers’ Share of Output

Consider Gindin’s response to the evidence that employee compensation was basically constant as a share of output. Gindin does not dispute this evidence. Instead, he disregards it, and substitutes a statistic that seems to contradict it: “between 1982 and 2007, the cumulative increase in hourly compensation in the nonfarm business sector (35%) totalled less than half that of productivity (75%).” In a recent article published in Truthdig, I explained why this supposed “productivity/compensation gap” is just a misleading factoid produced by inconsistent adjustment for inflation. It does not shed any light on the distribution of output or income. In particular, as I pointed out, it does not mean that profits grew more quickly than productivity or that the profit share of output increased at the expense of the compensation share, Doug Henwood’s recent claim to the contrary notwithstanding.

Had Gindin taken to heart the evidence I put forward instead of disregarding it, he would have recognized that compensation per hour of work and productivity (output per hour of work) increased at basically the same rate. Since compensation was basically constant as a share of output, total compensation and total output increased at basically the same rate. It follows immediately from this that compensation per hour and output per hour also increased at basically the same rate.

Household Income

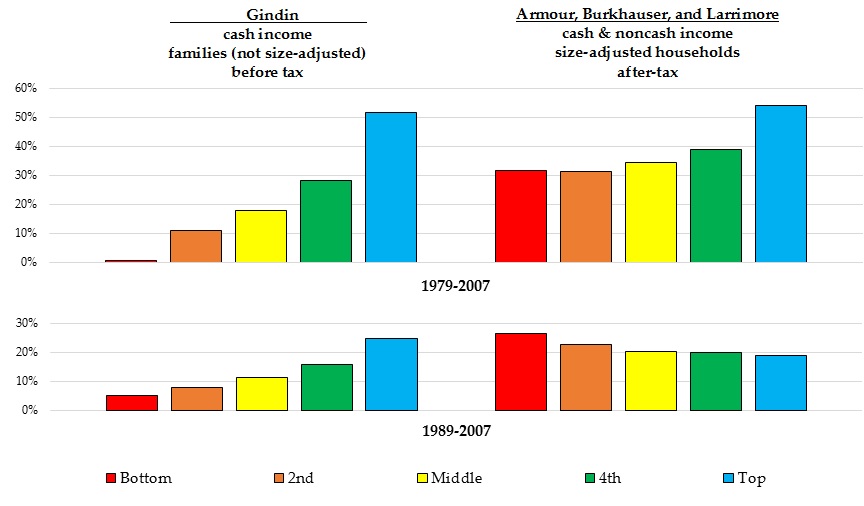

For another example, consider the evidence I cited, taken from a recent study by Armour, Burkauser, and Larrimore, that the incomes of lower and middle-income households grew substantially between 1979 and 2007 and that income inequality declined after 1989. Once again, Gindin ignores this evidence, and instead substitutes statistics that seem to contradict it. He tells us that “between 1982 and 2007, … while the bottom 80% of households saw their real income increase by 24% (i.e. less than 1% per year), the top 5% of households—generally not of the working class—saw an increase of 86%.”

This does not refute the evidence I provided. In the first place, although Gindin refers to “households,” the data he cites actually pertain to families.[5] The family statistics are increasingly unrepresentative. Last year, almost one in five Americans lived in non-family households; that is, they lived alone, in households headed by unmarried couples, with roommates, etc. Second, the data Gindin cites fail to count an increasingly important component of income––noncash income––which includes things like medical insurance benefits provided by government (Medicare, Medicaid) and employers, food stamps, and housing assistance. Third, these data fail to adjust for the sizable decline in household size that has caused income per person to rise more rapidly than income per household. Fourth, they pertain to before-tax income, while I was discussing after-tax income.

Figure 3 compares the figures that Gindin cites to the findings of Armour, Burkauser, and Larrimore.[6] They are strikingly different. The “Gindin” figures show much less income growth among the bottom three quintiles and they indicate that income inequality continued to increase after 1989. What accounts for these drastic differences? Both sets of figures make use of the exact same Census Bureau data on cash income, and they adjust for inflation in exactly the same way. Thus, the differences stem from the fact that Gindin cites data that ignore all noncash income, pertain to families, fail to adjust for changes in family size, and ignore the redistributive effect of the income-tax system, while Armour, Burkauser, and Larrimore count noncash income, look at households, adjust for changes in household size, and take the redistributive effect of the income-tax system into account.

Figure 3. Real Income Growth, U.S., by Quintile

Statements like “the bottom 80% of households [sic] saw their real income increase by 24%” are misleading because they wrongly present such figures as cut-and-dried facts. In reality, “by how much did their income rise?” has no answer; the question is too vague. An incredibly wide range of income-growth rates can be produced by varying the definition of “income” and the income-sharing units. For instance, Table 3 of the Armour, Burkauser, and Larrimore paper presents seven different measures of real income growth among the bottom quintile between 1989 and 2007, ranging from –32.9% to 29.4%! Thus, it will not do for Gindin to disregard the evidence I’ve presented and substitute his own as if that disposed of the matter once and for all. If he continues to insist, as he did in his initial article, that there was “stagnation of worker incomes” during the “neoliberal” era––and I should note that it’s quite a stretch to refer to his preferred figure for real income growth, 24%, as “stagnation”––he needs to tell us exactly what he is excluding when he refers to “income”, and he needs to provide cogent arguments as to why it should be excluded.

If one wants to argue, as he does, that neoliberalism smashed the working class, then all sources of income should be included. After all, if “the neoliberals” had succeeded in slashing medical benefits and other noncash income, this would certainly count as evidence that the working class was smashed. By the same token, the fact their overall noncash income was not slashed counts as evidence against that notion.

(The usual argument I’ve heard for why medical benefits should be excluded makes no sense at all. We are told that these benefits are not really income that accrues to working people, because Health Maintenance Organizations (HMOs) and other medical-service providers, not workers, receive the money that purchases these benefits. The same line of reasoning leads to the strange conclusion that cash wages which workers spend on bread is not really income that accrues to them, because capitalist baking companies receive the money that purchases the bread! To avoid this error, one needs to recognize that workers’ receipt of income is one thing, while the exchange of that income for goods and services (bread, medical benefits) of equivalent value is another thing. It also helps to think about what would happen if these medical benefits were taken away. Workers would be worse off, wouldn’t they?)

Increased Hours of Paid Work?

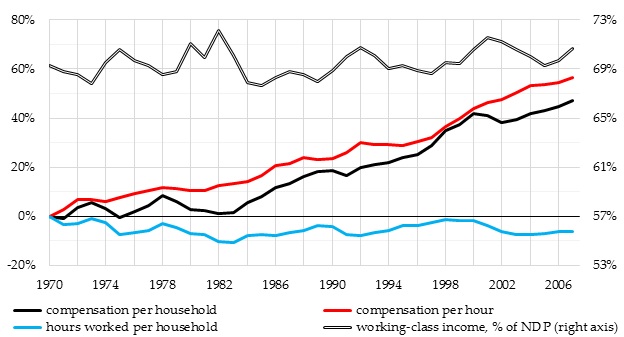

Gindin dismisses the evidence that working-class income trended upward as a share of net output between 1970 and 2007, as well as the evidence that the rise in the income of working-class households was nontrivial. He claims that these trends were “primarily due” to increased participation of women in the workforce; “the increase in household income … was based not so much on higher pay as on increased hours of paid work.” In other words, employee compensation per hour worked grew much more slowly than compensation per household; the faster growth of the latter was primarily due to household members working more hours rather than to an increase in compensation per hour worked.

This is simply not the case. As Figure 4 shows, hours worked per household actually declined. This means that none of the growth in employee compensation per household was due to increased hours of work. All of it—indeed, more than all of it—was due to the rise in compensation per hour worked, which grew more, not less, rapidly than compensation per household.[7] If we consider only the period from 1980 to 2007, hours worked per household were basically unchanged, which implies that compensation per household and compensation per hour increased at basically the same rate.

Figure 4. Employee-Compensation and Hours Worked, U.S. Households (percentage change since 1970)

The Decline in the Saving Rate

Gindin originally argued that workers managed to keep their standard of living from stagnating under neoliberalism by becoming “dependent on credit,” especially by “depend[ing] heavily on their homes as collateral for borrowings.” As he now acknowledges, my initial response showed that these statements are inconsistent with the evidence, at least prior to the home-price bubble that began in the late 1990s. However, he still denies that the rise in working-class income––employee compensation and net government social benefits––accounts for the fact that consumption spending by working people did not stagnate. The real explanation, Gindin contends, is that they increasingly depleted their savings: “the personal savings rate fell from over 11% in the early 80s to 3% in 2007.”

The main problem with this claim is that the rise in working-class income does account for the rise in working-class consumption. Between 1970 and 2007, working-class income trended upward slightly as a share of net domestic product (see Figure 4).[8] This means that working people, inclusive of the poor, were able to buy a bigger share of the product––without falling deeper into debt and without depleting their savings.

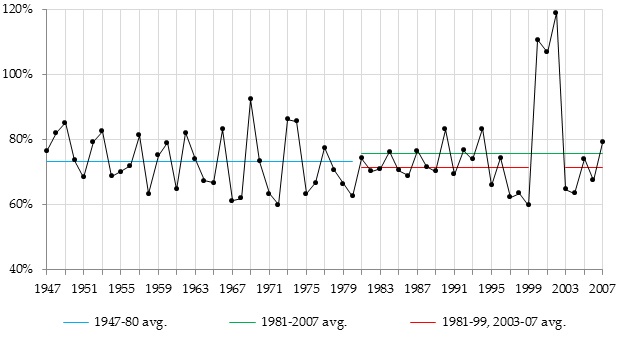

A secondary problem is that the decline in the saving rate is quite misleading because it fails to count increases in people’s wealth––the value of their homes, retirement portfolios, etc.––as additional income or saving. Thus, the saving rate that Gindin cites will fall if someone puts $1000 less of her current income into savings and CD accounts this year than she put in last year, even though her retirement portfolio increased by $2000 as a result of capital gains. Yet when increases in net worth are included as income, the fall in the U.S. saving rate disappears, as Figure 5 shows.[9] There was no discernible upward trend in consumption spending, and thus no discernible downward trend in saving, as a percentage of income inclusive of increases in net worth. Consumption spending as a share of this broadly-defined income was, on average, slightly higher between 1981 and 2007 than it had been between 1947 and 1980, but slightly lower once we omit the years 2000–2002. (That was when the dot-com bubble burst. Net worth fell by more than $4 trillion, which caused broadly-defined income to fall to 59% of its 1999 level.)

Figure 5. Personal Consumption Spending, U.S. (as percentage of after-tax income plus change in net worth)

Differentiation Within the Working Class

Gindin tells us that unionization rates fell and that “concessions were rampant in working conditions as well as wages.” This is correct, but it is also irrelevant insofar as the well-being of the working-class as a whole is concerned. As I noted in my initial response, “some parts of the working class suffered from ‘wage repression,’” but the notion that this was true “of the class as a whole” is just a pernicious myth. Only a relatively small minority of workers were unionized three decades ago and then “unionization rates fell,” so giveback union contracts had little direct impact on the working class as a whole. And any indirect impact they may have had was too small to offset the effect of factors pushing in the other direction. The evidence I put forward, which Gindin does not challenge, indicates clearly that working people’s wages and other income grew substantially.

Gindin also claims that “[n]eoliberalism demoralized workers” and “successfully lowered worker expectations,” but he provides no evidence to support these claims. They seem to be no more than personal impressions, and they are implausible. Women’s median wages rose by more than a third. Does Gindin really believe that, prior to the Great Recession, the expectations of working women—half the workforce––were lower than the expectations of their mothers and grandmothers a generation or two ago?

The strong growth of women’s wages is a clear sign that something is seriously wrong with the story that neoliberalism succeeded in smashing the working class as a whole. The exceptionally strong growth of income among older people is another. Three in ten U.S. seniors lived in poverty as recently as 1967, but fewer than one in ten does so today.[10] U.S. Census Bureau data indicate that, after adjustment for inflation, cash income of the median senior-headed household rose by 99% between 1967 and 2010, almost five times as fast as overall median cash income.[11] Since this figure pertains to median (middle) income, it is not being pulled up artificially by a relatively small percentage of wealthy seniors who live off of income from securities, lavish severance packages, and the like. The rapid growth of benefits received from Social Security (the government-run pension program) seems to be the dominant cause of the fall in seniors’ poverty rate and the rise in their cash income.

And if the working class as a whole was smashed by neoliberalism, then how did the wages college-educated workers rise so rapidly? A 2011 Congressional Budget Office study found that, between 1979 and 2009, the median inflation-adjusted hourly wage rate of men and women with a four-year college degree rose by 22% and 41% respectively. For men and women with some graduate education, the growth rates were 45% and 51%, respectively.[12] These figures include only cash wages, not noncash benefits, which probably increased even more rapidly, and they are for the median worker in each sex-education group, so they are not pulled up artificially by the high pay received by top executives, investment bankers, and the like.

As I wrote last year, in response to a Monthly Review article by Fred Magdoff and John Bellamy Foster that told a story much like the one that Gindin tells,

What we are left with is this. If wage trends can be adequately explained on the basis of a smashingly successful acceleration of the class war, it must be a class war only against younger, male, and less-educated workers, not a class war against older, female, and better-educated workers. But then it isn’t a class war. The alternative is that a class war is indeed being waged against the whole working class, but it wasn’t very successful, at least not insofar as wages and compensation are concerned, in the decades that preceded the Great Recession. Take your pick.

There is no doubt that the disproportionately male and white workers of working age who worked in union shops with seniority contracts took a big hit in the 1970s and 1980s as a result of giveback contracts and the flight of heavy industry to the South and overseas. But they were never the working class, and they are increasingly unrepresentative of it. The mental image of the U.S. working class that seems to grip much of the left––the socialist realist image of a young, muscled, male factory worker in overalls holding a hammer––was never accurate, and it has become less accurate over the years.

Thus, to understand the rise in income inequality that took place (to the extent that it did take place), we need to abandon the myth that companies’ profits rose at the expense of workers’ pay and focus on the increased differentiation within the working class that has occurred.[13] We also need to understand that interest and dividend income rose at the expense of corporations’ retained profits, not at the expense of employee compensation. And we need to understand that increases in capital gains generally boost the incomes of property owners without reducing workers’ share of output, because the capital-gain income does not come from output and is not a part of it.

Attitudes to Working People’s Thoughts

In my initial response to Gindin, I noted that a recent poll found that a large majority of black people, a majority of people under 30, and almost half of low-income people and Hispanics had a positive perception of socialism. I then decried the fact that “most of the Left, including the ‘socialist’ Left, has … [not been] listening to the renewed aspiration for a socialist future.”

Gindin’s rejoinder exemplifies this problem well. “It will not do,” he writes, “to point to polls showing support for socialism …. In American discourse, ‘socialism’ means support for greater state intervention … [;] it hardly reflects an imminent challenge to capitalism either ideologically or politically.” But he provides no evidence that the poll respondents were actually just supporting greater state intervention. The pollsters did not bother to ask them why their perception of socialism is positive. They evidently didn’t care. I suspect that Gindin is just guessing.

But why does he guess that black people, youth, poor people, and Hispanics mean the same thing by “socialism” that the bourgeois media means? Why does he assume that they simply line up in favour of one of the prevailing alternatives that “American discourse” offers instead of thinking their own thoughts? Wouldn’t it be a good idea to find out what they actually think and to engage with them rather than writing them off from the start? Even if some or most of them were to begin by saying that they support state intervention, a deeper dialogue might well reveal aspirations for a different future that can be a basis for social transformation.

It is not surprising that pollsters don’t care what working people think, but when socialists and other leftists evince similar attitudes, it is cause for concern. Gindin laments the fact that “the left has generally made little progress in penetrating the working class.” Aren’t elitism and condescension a major reason for this failure? I wish I had a quarter for every time I’ve heard leftists speak about “raising consciousness” of other people, or leading them, or characterizing the problem the left faces as difficulty in “getting our message across,” or ascribing failures to other people’s “false consciousness.”

Gindin thinks I am overly optimistic. He takes issue with my comment that “[c]lass struggles, taking a variety of traditional and new forms, have accelerated throughout the world during the crisis,” responding that “[i]t will not do to point to sporadic struggles as signs of hope. These are of course encouraging but they do not begin to approach the scale of the problem the working class confronts.” Of course they do not. But I did not point to them as signs of hope; I pointed to them in order to warn about and oppose a key obstacle to self-development that these openings for social transformation face: “these struggles have been derailed and confined by attempts to integrate them into the anti-neoliberal-but-pro-capitalist project.” In political contexts, terms like “optimism” and “pessimism” are of little use to me. I think in terms of openings and possibilities, and what can be done to try to make them a reality.

The real issue here is not that I am optimistic while Gindin is pessimistic, nor is it that I “dangerously mislead[ ] on how difficult the political project of challenging American capital will be.” I certainly do not downplay the actual difficulties; I just don’t include the mythical economic success of neoliberalism or its mythical smashing of the working class among them. The real issue is that, despite these difficulties, I am in favour of socialist transformation in the here and now, while Gindin seems willing to stagify. His alternative to the “sporadic struggles” he dismisses is an “organised working class,” but evidently not working class organized to achieve its self-emancipation. It is to be organized in order to “threaten[ ] instability if governments don’t move to radically greater economic stimulus.” This is just another expression of the efforts to integrate mass struggles into the anti-neoliberal-but-pro-capitalist project about which I warned.

There is no surer road to failure than leftist attempts to use working people as muscle in order to achieve goals that are not their own. The left can assist their “sporadic struggles,” not by trying to lead them or use them, but by assisting them. Engaging with them theoretically in genuine two-way dialogue is particularly crucial in order for working people to develop themselves to the point where they can run society themselves and re-establish it anew.

[1] The disposable personal income and personal consumption expenditure figures come from National Income and Product Accounts (NIPA) Table 2.1, lines 27 and 29, respectively. I used the personal consumption expenditure price index, reported in NIPA Table 1.1.4, to adjust them for inflation. The inflation-adjusted home construction (residential investment) figures come from NIPA Table 1.1.6, line 13.

[2] The deficit is the difference between current expenditures and current receipts, reported in NIPA Table 3.3, lines 21 and 1, respectively.

[3] The profit data come from NIPA Tables 6.19B–D, line 1 (not Tables 6.17B–D as Gindin reported). The capital investment figures by which the profit is divided come from the Bureau of Economic Analysis’s Fixed Asset Table 6.3, line 2.

[4] I point this out in order to call attention to the standards Gindin employs when assessing whether evidence supports his claims, not because I accept his profitability estimates. They are rather problematic. The biggest problem is that, although he counts income that U.S. multinational corporations receive from their foreign subsidiaries as profit, he fails to count the multinationals’ investments in their subsidiaries as capital investment. In addition, his profit data are based on depreciation as reported by companies on their tax returns, not the Bureau of Economic Analysis’s estimate of the actual amount of depreciation, and he treats increases in the value of inventories as if they were profit. The Bureau of Economic Analysis makes an “inventory valuation adjustment” which removes that part of “profit.”

[5] U.S. Census Bureau, Historical Income Table F-3.

[6] The data used to construct the Armour, Burkhauser, and Larrimore series are reported in Table 1, col. 3, and Table 3, col. 3 of their paper. Their estimates of capital gains are controversial, so I have used their figures that exclude capital-gain income. When they include capital gains, the reversal of inequality after 1989 is much greater. Their figures and those cited by Gindin are adjusted for inflation by means of the CPI-I-RS price index.

[7] The employee-compensation data are reported in NIPA Table 2.1, line 2. I used the CPI-U-RS price index to adjust them for inflation. Hours worked by full- and part-time employees are reported in NIPA Tables 6.9B-D. The number of U.S. households is reported in the U.S. Census Bureau’s Historical Income Table H-1.

[8] My measure of working-class income is compensation of employees, plus government social benefits, minus social insurance taxes, figures for which are reported in NIPA Table 2.1, lines 2, 17, and 25, respectively. Net Domestic Product is reported in line 29 of NIPA Table 1.7.5.

[9] Disposable personal income and personal consumption expenditure figures come from NIPA Table 2.1, lines 27 and 29, respectively. Net worth of households and nonprofits is the difference between their total financial assets and total liabilities, which are reported in lines 1 and 25, respectively, of Financial Accounts of the United States Table L.100. For many years, data for households alone are unavailable.

[10] U.S. Census Bureau, Historical Poverty Table 3.

[11] U.S. Census Bureau, Historical Income Table H-10.

[12] (U.S.) Congressional Budget Office, “Changes in the Distribution of Workers’ Hourly Wages Between 1979 and 2009,” Table 2, p. 8.

[13] It is frequently claimed that increases in the compensation of top corporate executives (which is arguably mostly profit in disguise) was the main factor that kept average employee-compensation from falling. However, my estimate, based on data reported by Bakija, Cole, and Heim and other sources, is that rising pay of salaried managers in the top 1% of tax units reduced other employees’ share of net output by only 2/3 of one percentage point between 1979 and 2005. I am currently working on a paper that describes my estimation procedures.

Be the first to comment